“I’m PISSED. I'm making more profit than ever. Why am I running out of cash??”

John is the founder of a modest MSP with a handful of technicians and dozens of clients.

“I started this business because I love cybersecurity. But then all I did was sales. I hate sales! So I hired a sales person… let’s just say the sales hire didn’t work out, and now I’m more stressed than ever. My business isn’t making enough money. I’m unhappy. But I can’t let down my customers or team. I feel stuck.”

When you dig into John’s business, you’d be surprised to see that his sales hire was actually increasing both revenue and profit each month. However, his MSP was hemorrhaging cash.

John was starting to worry about making payroll. John postponed his plan to pay himself a dividend.

Why was John’s cash going down, even though his revenue and profits were going up? What caused this sales hire to be such a disaster? Isn’t it good to delegate things that you prefer not to do yourself?

Cashflow, not cash, is king

John was losing cash every month, even though his salesperson was adding new business that was increasing his bottom line.

John was about to learn a hard lesson:

Revenue is vanity.

Profit is sanity.

Cashflow is reality.

Businesses are programmed to think in terms of profit or even EBITDA. But the reality is that cashflow, not profit, is the oxygen that supports the life of your business.

The critical difference between large MSPs and small MSPs is measuring progress on cashflow, not profit, not EBITDA.

When your bank account goes to zero, you have no business. You can’t make payroll. Your technicians, whom you worked so hard to hire and retain, all leave. You can’t deliver for your clients without your techs. Your clients leave too. No one cared that your profit went up, because you still ran out of cash.

Small profit change, but huge cashflow change

A mentor of mine once told me that cashflow is like a megaphone: if you whisper into a megaphone, it produces a scream. A small profit change that goes into the cashflow megaphone produces a magnified cashflow change.

Let's say John’s business does $400,000 in profit on $1,600,000 in revenue, annually, with $1,200,000 in supplier payments. That means John did $2.8mm in cash transactions to earn $400k. This is a 7:1 ratio, meaning $1 of profit could affect $7 of cashflow!

And MSP businesses are typically considered higher margin. Outside of the MSP space, businesses might do only $160k in profit on the same $1.60mm revenue and $1.44mm, meaning they’re doing $3.04mm in cash transactions to generate $160k profit. This is a 19:1 ratio, meaning $1 of profit could affect $19 dollars of cashflow.

But what are the different ways that a small profit change can lead to a huge cashflow change in John’s MSP business?

What if John’s salesperson onboarded a client that increased revenue 10%, but all the client’s payments are on Net 90 terms?

What if John reduced the frequency of client cybersecurity audits from weekly to monthly, freeing up technician time to service this new large client, but reducing the opportunities to upsell cybersecurity services to all other clients?

What if John agreed to pay his new salesperson a commission for landing this new big client, even though the new client hasn’t made its first payment yet?

All of the above could have a long-term cashflow impact an order of magnitude larger than the profit impact.

John was pushing his business to increase its revenue and profit, but the unforeseen cashflow decrease suffocated his business anyway.

How large MSPs optimize for cashflow (which you should copy)

I’d like to introduce you to the 13-week cashflow forecast. It’s a weekly ritual to optimize cashflow for your business by reviewing variances between forecasted cashflows and actual cashflows.

The gist is to take the current cash balance, forecast the receipts and payments for each of the next 13 weeks, and update your forecasts each week. The usefulness of your cashflow forecasts depends on the quality of your predictions.

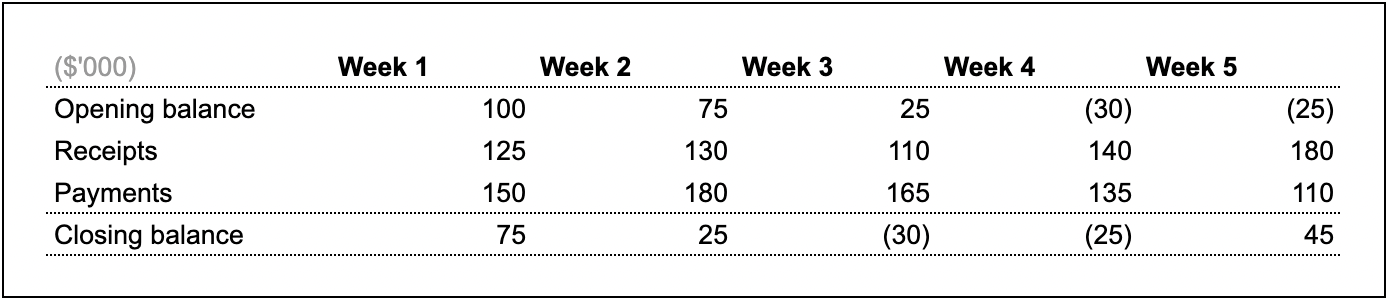

Here's a simple example:

A simplified weekly cashflow forecast

This example forecasts that weeks 3 and 4 will be a cash deficit. This hypothetical business has options to fund this deficit:

A cash investment

An overdraft facility (i.e. a temporary loan)

The deferral of payments due during and before the weeks with a deficit, weeks 3 and 4

The acceleration of receipts that arrive after the weeks with a deficit, week 5

To be useful for your own business, your cashflow forecast should be more specific with the sources of receipts and destination of payments. Then you can use your cashflow forecasts to inform management decisions.

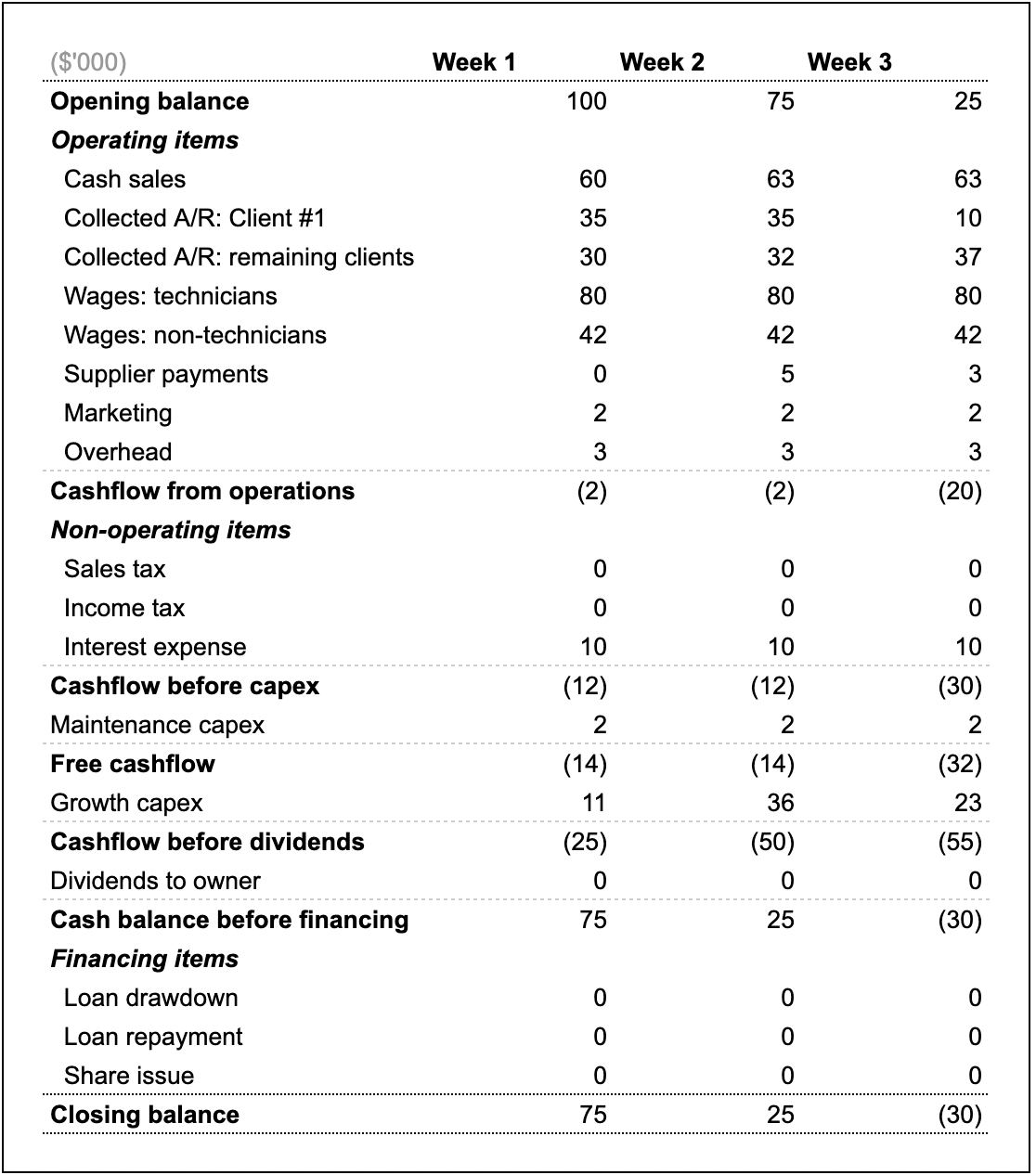

Here's a more realistic example to illustrate this added complexity:

A more detailed weekly cashflow forecast

Note that this example goes to only 3 weeks to make the example more legible for yourself, the reader. When you implement your own forecasts, they should go out to 13 weeks.

How does the 13-week cashflow forecast help MSPs?

The top benefit is that your business adopts a cashflow culture. Revenue is vanity, profit is sanity, cashflow is reality.

What you make what you measure. So if you want to improve your business’s reality, build a cashflow culture to measure and maximize cashflow.

As a result of a culture around cashflow instead of profit or revenue, working capital efficiency becomes top of mind for your whole team, and any cashflow inefficiencies in your business will reveal themselves to you quickly.

5 steps to setting up your MSP’s 13-week cashflow forecast

You don’t need a professional CFO to do it for you, but it’s not an overnight project either. You’ll need to set aside time to setup the process, plus carve out weekly time to run the process.

1. Pick the rows to put into your cashflow forecast

The forecast reads similarly to a P&L and has a row for each cashflow variable, but the specific rows vary per business. Each row in your cashflow forecast should be a cashflow variable in your business that is worth your weekly scrutiny.

For instance, you might have one or two big clients who pay the majority of your revenue, but their payments might be irregular. If this introduces cashflow risk that’s worth your weekly scrutiny, then you could create individual rows for sales receipts for each big clients.

Pick a forecasting methodology for each row, including how to forecast it, and how frequently you’ll re-forecast each row.

2. Decide the owner for your 13-week cashflow forecasting process

This is a weekly process, so someone in your organization needs to be accountable for running the process and driving to its intended results. Unless the MSP owner delegates this to someone else, like a dedicated controller hire or a 3rd party CFO, it will fall upon the MSP owner themself.

At larger MSPs, the owner of their cashflow forecasts would be their controlling team.

3. Every single week, run your cashflow forecasting process

There are three dimensions by which you should scrutinize your cashflows:

The actual cashflow from last week vs the forecasted cashflow for last week. What forecasts didn’t manifest as predicted, and what caused the variance? How can you reduce the variance between actual and forecast next time?

The latest forecasts. Which rows are you re-forecasting this week, and what’s causing your re-forecast decisions for each row?

The latest forecast vs your previous forecast. Which rows have updated forecasts, and what’s causing the variance? How can you improve your forecasting methodology?

We advise the owner of the cashflow forecasting process to reconcile the previous week’s bank transactions and actualizing last week’s cashflows by Monday, then completing the forecast by Tuesday.

4. Iterate on your cashflow forecasting methodology over time

You can consolidate rows if they don’t provide value by being broken out, or break out a row into multiple rows if zooming in is useful.

You can revisit your re-forecasting methodology and frequency for each row.

5. Show your team how they impact cashflow

Your entire team makes small decisions each day which impact cashflow. Each team member affects at least one of the rows in your forecast. Show how each teammate’s impact is increasing or decreasing each row.

When everyone sees a cashflow number that they are impacting, they’ll align with you to improve that cashflow number and increase your MSP’s cashflow.

Reference your cashflow forecasts anytime your leadership is making a decision. Each decision should aim to optimize cashflow.

Downsides of the 13-week cashflow forecast

The 13-week cashflow forecast is the first step that any small MSP should take if it aspires to grow into a large MSP. It’s unlikely to be the only step, and here’s why.

It’s only useful for up 13 weeks

Our cashflow forecasts don’t interact with your financial statements, which you’ll still need to close your books at your regular cadence, which is monthly for most MSPs. You can’t use these forecasts for longer time horizons, and it’s difficult to rely on the 13-week cashflow forecast to inform bigger decisions that will impact cashflow beyond 13 weeks.

This means that 13-week cashflow forecasts aren’t a great tool to assist with capital allocation decisions. Let’s say your MSP is made an extra $10k. How can we allocate this $10k to maximize cashflow? Is it another technician? A sales hire? Adwords? Most of these capital allocation decisions will impact you beyond 13 weeks, which means you’ll need a different tool to inform your decisions.

The solution to this would be to implement 18-month cashflow forecasts, which is much more complicated to setup and understand. You’ll certainly need a strong CFO on your side to set it up, but you’ll unlock the ability to make longer term decisions based on longer term cashflow forecasts. But this is a post for another day.

The risk of double count or omission

Some rows are easy to forecast because they’re based on your receivables and payables ledgers. They’re easy to forecast because we’re just predicting the cash settlement of sales and purchases that already happened.

However, the further in the future we’re forecasting, the less likely we can rely on our receivables and payables ledgers for forecasting. A forecast for week 13 might rely on transactions that will occur in week 7 or week 10, but a week 1 forecast could rely exclusively on the receivables and payables ledgers.

So your team has to have a well-founded methodology for forecasting future sales and purchases. And then your forecasting process needs a smooth hand-off process, to transition from the receivables and payables ledgers to forecast sooner weeks, to the sales and purchases forecasting methodology to forecast the later weeks.

The timing of actualization

Your forecasts won’t be reliable if the actualizations consistently vary dramatically from forecasts.

Let’s say a customer agreed to pay you $1k per month. However, you gave them a discount for next month for 50% off, so you’ll earn $500 from this customer for next month. You’ll need to adjust your forecast so there’s $500 less after a month.

Now try adjusting for any timing differences in actualizing cash settlement for any transactions. What if you paid out a sales commission for a new client which hasn’t made its first payment yet? What if some vendors gave you temporary discounts, but their discounts all work differently, and extend across different time horizons?

We always advise MSP owners to prioritize growing MRR over all other kinds of revenue. Assisting with predictable cashflow forecasting is a huge reason why acquirers will pay a premium to acquire in an MSP instead of another business, but that makes sense for the acquirer only if they’re acquiring an MSP with most of its revenue being MRR.

But selling your MSP is a post for another day.

Summary

Focus your business on growing cashflow, not revenue or profit or EBITDA. Revenue is vanity, profit is sanity, cashflow is reality.

The 13-week cashflow forecast is the most important habit of large MSPs that small MSPs don't do. If there's one strategy that small MSPs should copy from large ones, it's this one.

If you don't have a 13-week cashflow forecast, start immediately! Email me [email protected] with questions if you'd like to chat about it.